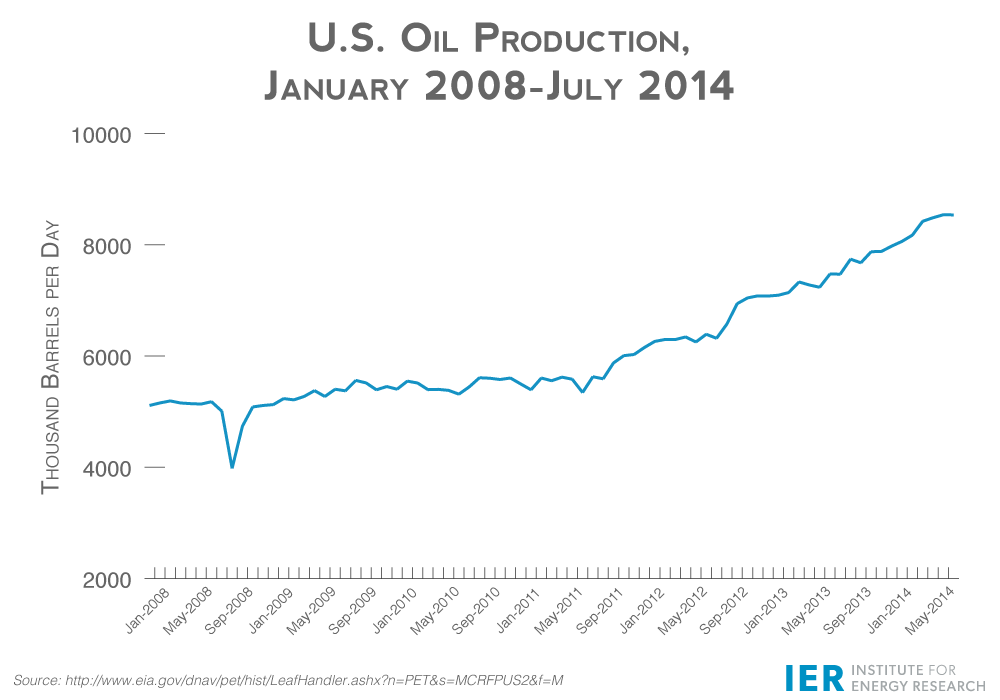

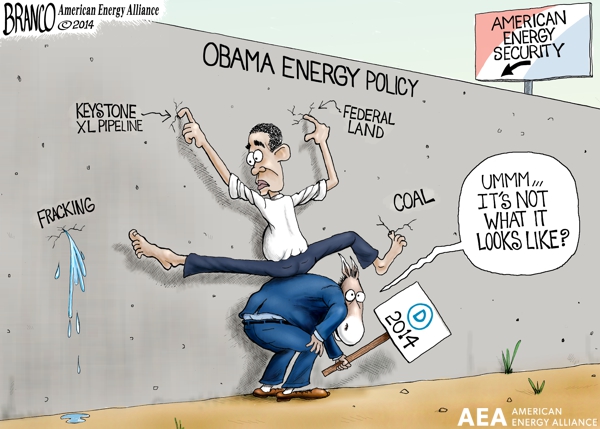

During the lame duck session, one of the top priorities for President Obama and Majority Leader Reid is the passage of a tax extenders package that includes a retroactive extension of the decades old wind production tax credit (PTC). The PTC is a key part of President Obama and Majority Leader Reid’s attack on affordable energy from natural gas, coal, and nuclear. We urge you to reject any attempt to revive the PTC.

First, it makes no sense for the Republicans to give away any leverage they may have with respect to tax reform in the 114th Congress. Calls to “clear the decks” for the new Congress are nonsensical; why would the newly elected Senate and House members (from either party) want to reward Senator Harry Reid for his legacy of dysfunction by allowing him the opportunity to advance his pet priority—the wind PTC—during a lame duck session?

Second, extending the PTC restricts Americans’ access to affordable and reliable energy. The PTC harms Americans in two important ways: it hides the true cost of wind power and encourages states to keep expensive wind power mandates. This makes it easier for the President to promote his restrictions on carbon dioxide emissions from existing power plants because the PTC hides the true costs from ratepayers.

Third, the PTC enables wind operators to use the tax code to engage in predatory pricing against reliable and affordable nuclear, coal, and natural gas power plants. The PTC is such a large subsidy that industrial wind facilities can actually pay the electrical grid to take their electricity and still make money. This predatory pricing is designed to drive nuclear, coal, and natural gas generators out of business and it is only profitable because of the PTC.

If you favor substantive, meaningful tax reform, you should oppose the inclusion of the PTC in any lame duck tax extenders package. Rejecting efforts to extend the PTC is a meaningful way for this Congress to oppose the President’s climate plan. A vote for extending the PTC is a vote for the President and the Majority Leader’s agenda.

Click here to see the full letter.

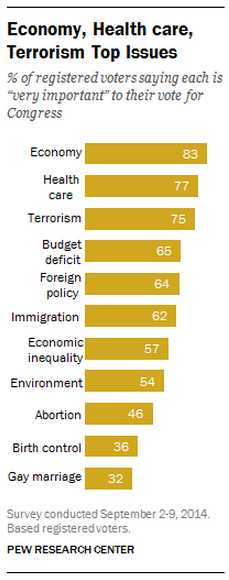

These results square with a poll AEA conducted, which revealed that economic and fiscal issues still reign supreme over environmental and climate issues. AEA found:

These results square with a poll AEA conducted, which revealed that economic and fiscal issues still reign supreme over environmental and climate issues. AEA found: